Does CRE deliver too little return?

It is often argued that the property market offers too weak a risk-adjusted return, particularly because interest rates have risen faster than property yields. But does that give the full picture?

When assessing expected returns going forward, it is useful to compare real estate with other asset classes, both in terms of historical performance and future expectations. It is important to maintain a measured perspective, avoiding too much influence from the exceptionally strong capital markets we have experienced in recent years.

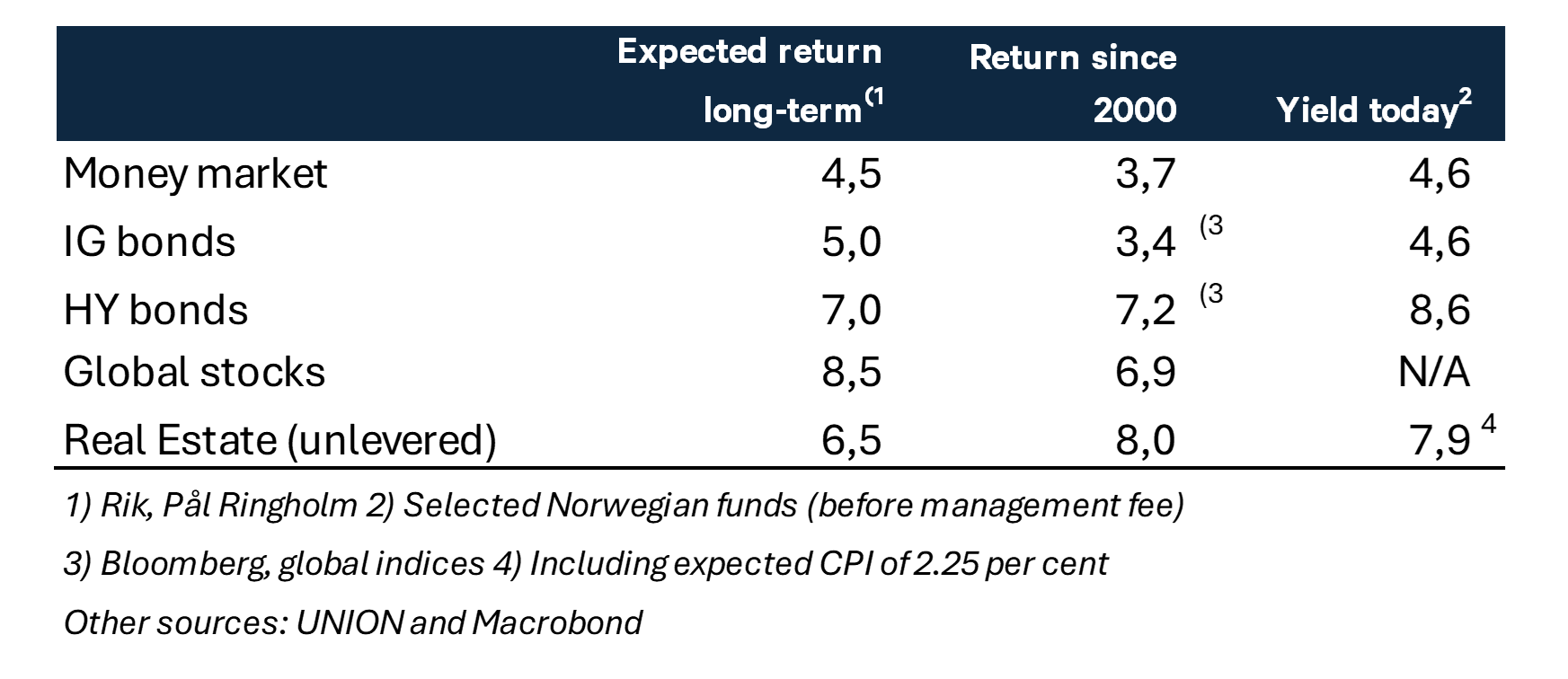

The table presents key figures across various asset classes. In the first column, we show typical long-term return expectations, while the second column presents actual returns since 2000, the year MSCI launched its index for the Norwegian property market. The index shows an average annual unlevered return of around 8.0 per cent over the period.

Over the same period, the Oslo Stock Exchange delivered a return of 9.6 per cent, while the global equity index returned 6.9 per cent. Both the money market and bond investments have delivered slightly below par over the period, largely due to the low-interest rate environment that prevailed for much of the time.

In the final column, we show the current yields from various fixed-income and real estate funds. This is not necessarily the same as expected returns. In the property market, the key factors will be the development in rental levels and asset values, while bond funds are influenced by credit losses and changes in interest rates and credit spreads. For a broadly diversified portfolio, however, these levels still provide a reasonable indication of valuation and what constitutes a realistic long-term return.

Looking at property funds with solid portfolios and broad exposure, we estimate an average yield of around 5.65 per cent. These portfolios typically consist of office, logistics, hotel, and retail properties. Since cash flow normally increases with CPI on an annual basis, we have adjusted for this in our calculations.

An important question is which inflation rate one should use as a basis. If we refer to the central bank’s inflation target of 2.0 per cent, this would imply a total return of 7.65 per cent. However, there is good reason to assume that inflation will remain somewhat higher in the years ahead. According to forecasts from Statistics Norway (SSB) and several major banks, inflation is expected to be closer to 2.5 per cent, at least through 2028. In the table, we have assumed 2.25 per cent.

A small percentage point is then lost to depreciation and maintenance (capex). At the same time, the strong increase in construction costs and higher interest rates means that the current stock of buildings appears undervalued relative to replacement cost. This suggests that rents could potentially grow slightly faster than CPI in the coming years.

Looking at the bond market, investment-grade funds currently offer an effective yield of just above 4.6 per cent. High-yield funds offer higher returns at around 8.6 per cent, but when adjusted for credit losses, it is reasonable to assume a net long-term return in the range of 7 to 8 per cent.

In other words, the “expected return” in the real estate market is roughly 2.5 percentage points above that of a typical investment-grade fund, and not far from the level of high yield. In essence, this is entirely in line with what one would expect.

What happens in the equity market in the coming years is, of course, impossible to predict. Based on historical performance, however, it seems unlikely that equities will deliver more than 8 to 9 per cent over the long term. And given today’s valuation levels, the balance of risks may in fact be tilted to the downside - particularly for US equities, which carry significant weight in global indices.

But ...

At today’s interest rate levels, leveraged real estate investments – which still make up the majority - deliver weaker returns than we became accustomed to during the low-interest era. Using the same MSCI index and adjusting for leverage, or based on other performance data, it has not been uncommon to achieve annual returns of 15 per cent or higher.

Finding investments that deliver such returns at today’s borrowing costs is clearly challenging. This naturally places greater demands on managers, who must now generate outperformance primarily through active management rather than through financial structuring.

In other words, it is true that property yields in many cases no longer reflect borrowing costs as they once did. But it is equally true that real estate as an asset class often still delivers competitive returns. And even if leveraged investments no longer perform as well as they used to, you would be hard pressed to find other asset classes with a reasonable risk profile that offer 15 per cent returns either.